By 2050, the child born this Raya will be sitting where we are sitting now, He will be making decisions, paying taxes, raising children of his own. What we build in the next two decades, or fail to build, is the inheritance we leave them. Net zero is not a KPI on a government scorecard. It is a debt we owe to people who are not yet old enough to collect it. The climate will not wait for better timing. It will simply move on without us.

Which makes what Malaysia has built so far both genuinely impressive. But it is not enough. Not yet.

The National Energy Transition Roadmap, launched in 2023, is one of ASEAN’s most structured transition architectures — a document that names sectors, assigns levers, sets timelines, and acknowledges the financing gap in the same breath as the ambition. For a middle-income economy still expanding its industrial base, that level of specificity deserves honest recognition.

A blueprint is not a building.

The levers are named. Some are moving. Some are stalled. The gap between what the roadmap envisions and what the ground is delivering is precisely where the real risk lives — not in the ambition, but in the architecture of execution.

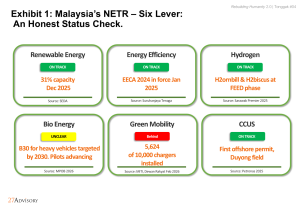

The Six Levers: An Honest Scorecard

Malaysia’s transition architecture rests on six levers. They are not moving at the same speed.

Renewable energy leads with measurable momentum, supported by global analysis. The UNEP Emissions Gap Report 2024 identifies solar and wind deployment as capable of providing 27% of total mitigation potential by 2030, using technology commercially available today. Energy efficiency and CCUS have moved from policy into legislation. Hydrogen is in engineering design phase. Green mobility is the clearest gap. Bioenergy carries the most uncertainty. Malaysia’s biodiesel mandate has progressed to B10 nationwide. Pilots toward B20 are advancing in select locations. The NETR targets B30 for heavy vehicles by 2030, conditional on economic viability. That threshold has not yet been reached.

The Lessons We Have Not Learned Yet

Malaysia is not navigating this transition without a map. Other economies have already begun to mark the terrain.

Shanghai: The Case for Cluster-Level Precision

Shanghai’s most instructive contribution is not its scale. It lies its architecture. Rather than applying blanket national policy across all industries simultaneously, Shanghai assigned dedicated frameworks to specific industrial clusters. The Lingang Special Area operates under its own hydrogen scale-up pilot. The Shanghai Chemical Industry Park runs dedicated sub-parks for carbon utilisation in key materials sectors. The lesson is not that China moves faster. It is that China moves specifically.

For Malaysia, the question is whether Penang’s semiconductor corridor, Johor’s industrial development region, and the East Coast Economic Region can each receive transition frameworks as precise as the industries they contain. A national roadmap is necessary. Cluster-level precision is what converts it into results.

Singapore: The Credibility of the Signal

Singapore’s carbon tax stands at S$45 per tonne of CO2-equivalent as of January 2026, covering approximately 70% of national emissions. It will rise to between S$50 and S$80 per tonne by 2030. What makes Singapore’s approach instructive is not the rate. It is the published schedule that industries can plan against with certainty. Singapore also built transitional protections for emissions-intensive, trade-exposed sectors, absorbing competitive risk while green alternatives matured.

Malaysia is building toward the same clarity. The foundations are being laid, though not yet set The National Climate Change Bill remains under review as of March 2026. The carbon tax intent is confirmed for the iron, steel, and energy sectors. The legal architecture that would give it binding force is not yet in place. That gap between announcement and legislation is not a minor administrative detail. It is the difference between a price signal and a policy aspiration.

The Three Gaps That Determine Everything

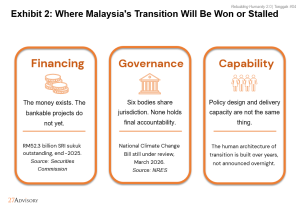

Three structural conditions will determine whether Malaysia’s six levers move at the speed the roadmap requires. They sit beneath every lever simultaneously.

Financing: The Bankability Problem

Outstanding sustainable and responsible investment sukuk reached RM52.3 billion by end-2025, rising from RM5.3 billion in 2020. The money is not the constraint. Anchor investments are moving. TNB’s RM43 billion grid modernisation and RM16.5 billion in GLC commitments for 2026 confirm this. The gap sits in the middle layer: industrial retrofits, emerging grid technologies, and the transition finance mid-sized manufacturers need to move from brown to green. The AIIB said plainly in Kuala Lumpur, February 2026: the capital exists. The structured, de-risked projects do not yet exist in sufficient number to absorb it. Malaysia’s Corporate Green Power Programme sketches a viable pathway. Structured voluntary procurement, anchored in long-term contracts, is what converts intent into investment.

Governance: Six Bodies, No Coordinator

Malaysia’s energy transition is overseen by at least six bodies with overlapping jurisdiction: the Ministry of Energy Transition and Water Transformation, the Ministry of Natural Resources and Environmental Sustainability, the Economic Planning Unit, the Sustainable Energy Development Authority, the Energy Commission, and state governments. No central coordination unit exists. The consequence is not dramatic failure. It is something quieter and more expensive: delay, duplication, and a private sector that learns to wait rather than commit. When accountability is distributed across six institutions, capital does not disappear. It relocates to jurisdictions where the pathway is legible. This is not a failure of effort. These bodies are executing their mandated roles within a structure not designed for the speed this transition demands. The design is the problem. And design can be changed.

Capability: The Human Architecture

The distance between policy design and delivery capacity is where transitions quietly stall. Malaysia already produces the talent this transition requires. The harder question is retention. When a green infrastructure engineer or a carbon markets specialist can earn three times the salary across the Causeway or in Melbourne, the capability gap compounds quietly. It is not from absence of talent, but from absence of the conditions that keep it here. Indonesia’s Rimba Raya Biodiversity Reserve, which has prevented over 130 million tonnes of CO2 emissions through REDD-style forest conservation, was built on exactly the kind of MRV expertise and institutional capacity that Malaysia’s ecological base is ready for, but has not yet assembled.

The urgency is not Malaysia’s alone to feel. The UNEP Emissions Gap Report 2024 estimates annual mitigation investment must rise to $5-7 trillion which is roughly five times current levels. The private sector is already responding: Shell committing $10-15 billion to low-carbon solutions, Maersk ordering 25 new vessels capable only of running on green fuels, Michelin targeting 40% renewable materials in every tyre by 2030, Holcim producing 8 million tonnes of net-zero cement annually through seven CCUS plants. These are not pledges. They are capital commitments with published timelines. The industries serving Malaysia’s economy are already repricing carbon into their cost structures. The question is whether Malaysia’s regulatory architecture will be ready when they arrive at the door.

The Execution Test

Malaysia’s clean energy advantage is real. It is also unfinished.

The ASEAN region is not waiting. Cross-border electricity trade, green hydrogen export corridors, and the architecture of a regional power grid are moving from policy documents into commercial conversations. Malaysia carries genuine advantages: resource endowment, an established capital market, a structured roadmap, and a geographic position at the centre of regional energy flows.

Advantages are not outcomes. They are starting positions.

First-mover advantage is not awarded to the best-resourced country. It is awarded to the one that can execute before the window narrows.

But execution was never the government’s alone to carry.

NETR is not a government document. It is a national contract. And every Malaysian is a signatory, whether they know it or not. Every EV purchased instead of a petrol car. Every rooftop solar panel. Every procurement decision that weighs carbon alongside cost. These are not gestures. They are the aggregate that determines whether the roadmap stays a document or becomes a country. The rakyat are not the audience of this transition. They are its co-authors.

Twenty-four years. One inheritance. Build it well.

A note on sources: This assessment draws on publicly available data as of March 2026. Implementation on the ground may exceed or fall short of what current reporting captures. 27Advisory has made every reasonable effort to trace and verify the figures cited in this article.

This article is part of 27Advisory’s Rebuilding Humanity 2.0 framework, a nine-pillar knowledge architecture for navigating Malaysia’s most consequential structural transitions. The themes explored in this piece connect directly to Pillar #05: Infrastructure, Water & Climate Resilience. This pillar examines how Malaysia builds the physical and institutional foundations required to absorb climate shocks while capturing the clean energy opportunity. To explore 27Advisory’s sectoral research and advisory work, please visit here https://27groups.zoholandingpage.com/rebuildinghumanity2dot0/ & drop us an email.